Regulations can be shaped and changed according to technological innovations and the geopolitical situation. Regulatory bodies aim to have an equal area of practice for everyone. It creates new rules by changing the existing laws to involve everyone in the game. In addition to being aware of these rules before, understanding these rules' content is essential in the harmonization process.

The Financial Crimes Enforcement Network (FinCEN) has performed the CDD Ultimate Rule published by the U.S. Department for Financial Institutions in May 2018. The CDD Final Rule includes a set of new Customer Due Diligence requirements crucial for AML solutions for banks. To comply with these regulations and the necessities of CDD rules, anti-money laundering compliance software became more important for companies.

What is Customer Due Diligence Final Rule?

The CDD Final Rule was by the U.S. Treasury Department's FinCEN to ensure that banks, brokers, insurance companies, real estate, and other compulsory financial institutions have usufruct benefits for their corporate clients.

To be more precise, the CDD Final Rule's application is necessary to determine which under the companies' control financial institutions are affiliated and reveal their relationship with criminal activities such as money laundering and terrorist financing. CDD Final Rule is a solution to understanding the precision of forward-looking processes and systems. Other CDD Ultimate Rule objectives are to strengthen and clarify the CDD requirements of banks and expose money laundering risks and terrorist financing by ensuring that financial institutions cannot conduct a risk assessment for legal entities and institutions' dependents. Anti-money laundering compliance software solutions, especially for banks, insurance companies, real estate agents, etc., support companies to conduct a comprehensive CDD procedure by automating processes.

What Changes to Expect in CDD Final Rule

Since its introduction, the CDD Final Rule has undergone some changes and updates, affecting AML solutions for banks and other institutions using technological solutions. Financial institutions need to keep up with these changes to ensure they remain compliant and avoid potential fines or other penalties. Here are some changes to expect in the CDD Final Rule:

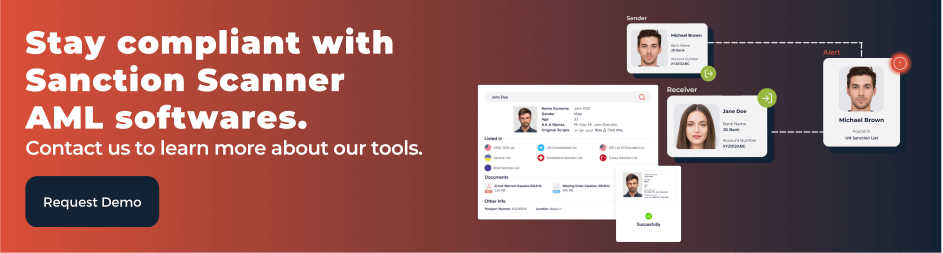

- Expanded definition of beneficial owners: In 2021, FinCEN announced that it would be expanding the definition of beneficial owners to include "entities" such as trusts and shell companies. This change will require financial institutions to collect additional information to identify and verify the beneficial owners of these entities. Anti-money laundering compliance software used by banks and other financial institutions can screen records and check UBOs for financial institutions.

- Streamlined certification process: The CDD Final Rule requires financial institutions to certify that they have collected and verified the necessary information about their customers' beneficial owners. In 2020, FinCEN provided guidance on streamlining this certification process by allowing financial institutions to rely on information provided by third-party service providers.

- Enhanced customer due diligence: Financial institutions are required to conduct ongoing monitoring of their customers to detect and prevent suspicious activities. In 2020, FinCEN provided guidance on enhancing due diligence (EDD) by recommending that financial institutions collect additional information on their customers' sources of funds and the purpose of their accounts.

- Risk-based approach: The CDD Final Rule emphasizes a risk-based approach (RBA) to identifying and verifying the identity of customers and beneficial owners. Financial institutions are expected to conduct a risk assessment of their customers and tailor their due diligence procedures accordingly. In 2021, FinCEN released guidance on how financial institutions can effectively manage their risk assessments.

Principles of CDD Final Rule

According to FinCEN, there are four significant factors for Customer Due Diligence:

- Get to Know Your Customer (KYC) and Authenticate.

- Determine if your customer has the usufruct right.

- Identify your customer's risk profile with an accurate customer risk assessment.

- Comply with a risk-based process to ensure that your risk situations are continuously reported.

- Ultimate Beneficial Owner (UBO) Practices

Organizations need to be UBO-compatible with professional businesses to access the source of information. The basic principles that AML professionals must follow when preparing procedures and collecting UBO information are as follows:

- Timelines

- Identification and verification of customer

- Make sure the business management of the vendors

- Making regular risk assessments and Taking measures against potential risk situations.

- Determine the usufruct rights of the customer.

The fact that businesses do not face money laundering risks and be instantly informed about the necessary aml regulations ensures that they protect their reputation. That's why accessing UBO information is an essential thing for professional organizations. With these steps, you can make your company's compliance program robust and scalable.

Importance in the Fight Against Financial Crime

CDD Final Rule requires financial institutions to identify and verify the identity of the beneficial owners of their clients. Beneficial owners are individuals who ultimately own or control a legal entity or arrangement, such as a company or trust. By identifying and verifying beneficial owners, financial institutions can better understand the true ownership structure of their clients and identify any potential money laundering or terrorist financing risks.

Also, CDD Final Rule emphasizes the importance of conducting ongoing monitoring of clients' transactions and activities to detect and report suspicious activity. AML solutions help banks and other companies to implement these measures. Financial institutions are required to establish and maintain risk-based procedures for monitoring their clients' transactions and activities, including the transactions of their beneficial owners. By doing so, financial institutions can identify and report suspicious transactions in a timely manner, which can help prevent money laundering and terrorist financing.

It applies not only to banks but also to other types of financial institutions, such as broker-dealers, mutual funds, and insurance companies. This means that a wide range of financial institutions must comply with the CDD Final Rule and implement effective customer due diligence procedures.

Lastly, Anti-money laundering compliance software are crucial to prevent money laundering and terrorist financing, including customer due diligence, transaction monitoring, and reporting suspicious activity. By complying with AML regulations, financial institutions can help protect the integrity of the financial system and prevent criminal activity. the compliance can be supported by in-house systems, manually or a professional Anti-money laundering compliance software. Companies must have one of them according to their size, needs and sector.