Ultimate Beneficial Ownership (UBO) is the individual or entity that ultimately owns or controls a company, partnership, trust, or other legal entity. UBO identification is a critical component of Know Your Business (KYB) and Know Your Customer (KYC) processes, and financial institutions such as banks, investment firms, and insurance companies are required by regulators to identify and verify the UBOs they do business with.

The reason for this requirement is to prevent serious crimes such as money laundering and terrorist financing. When UBOs are not disclosed, it creates an opportunity for individuals to launder money through the company. Therefore, countries should prioritize UBO identification to combat these types of financial crimes. By properly identifying UBOs, financial institutions can take appropriate steps to mitigate the risk of illicit activities and ensure compliance with regulatory requirements. Today, different AML software solutions help companies identify and screen UBOs in the sanction, watch, or PEP lists.

Who is the Ultimate Beneficial Owner (UBO)?

The most common UBO, or Ultimate Beneficial Owner, meaning refers to legal entities or individuals that ultimately possess control over a company, serving as its legal owners or entities. The role of UBO can be described as follows:

- People who have at least a 25% stake in the capital of the legal entity

- People who have at least 25% voting rights in the general assembly.

- People who are beneficiaries of at least 25% of the capital of the legal entity

Financial Action Task Force (FATF) and the European Union agree that working with third parties and their Ultimate Beneficial Owners increases the risk of facing financial crimes such as money laundering and terrorist financing. AML regulations include ultimate beneficial ownership and know your business regulations for all financial institutions. The EU released the Fifth Anti-Money Laundering Directive (5AMLD) to make financial transactions more transparent. According to 5AMLD, UBO screening must include senior managers and higher ranks. A powerful AML software tool can screen all these titles in the related lists.

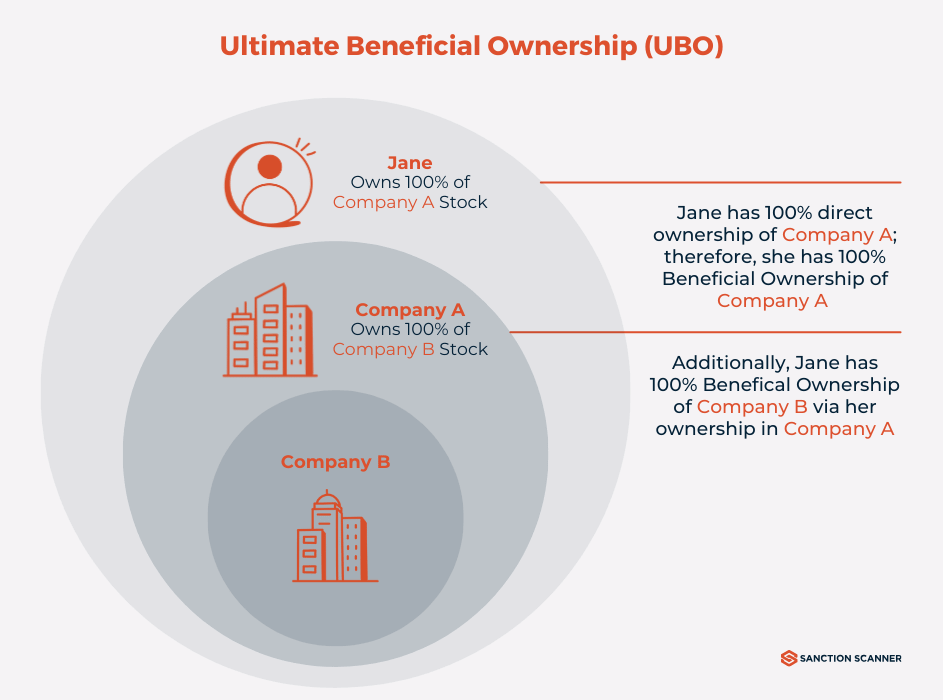

The Ultimate Beneficial Owner refers to the person or entity that is the ultimate beneficiary when an institution initiates a transaction. The beneficial owner is the natural person who, ultimately, is the person on whose behalf a transaction is conducted. It also includes those persons who exercise ultimate effective control over a legal person or arrangement.

The issue of UBO or controllers has become more critical internationally: it plays a central role in transparency, the integrity of the financial sector, and law enforcement efforts. Beneficial owners are always natural persons who ultimately own or control a legal entity or arrangement, such as a company, a trust, a foundation, etc.

Is Ultimate Beneficial Owner Scan Mandatory for Companies?

Reputation is significant for companies because their reputation affects customers' trust in the company. Therefore, they want not to be on the agenda with bad news and protect them from the factors that will cause reputational damage. Collaborating with fraudulent companies or not meeting AML requirements will cause them to face fines. This leads to the loss of the company's reputation.

One way to avoid this is to do a UBO scan. It is a mandatory process for companies that are responsible for anti-money laundering and counter-terrorist financing laws. The companies check the counter company's directors by scanning the UBO in their business agreements with AML software. This screening determines whether the company's owners or shareholders will pose a problem for them. Companies performing know your business controls, Customer Due Diligence (CDD), and UBO scanning may decide not to make business deals with high-risk companies to maintain their corporate reputation.

Companies that do not perform Ultimate Beneficial Owner scanning face various risks. Failure of a company to carry out UBO checks causes it to fail to detect risks. For this reason, they may cooperate with criminals or fraudulent individuals without realizing them and may harm the company's reputation. In addition, those who do not perform UBO checks are punished by regulators according to AML laws if they are under the AML / CFT obligation.

What are the Risks of UBOs for Companies?

UBOs are the individuals or entities that ultimately own or control a business or organization. While UBOs play an important role in corporate structures, they can also pose significant risks for those companies, particularly regarding money laundering and other financial crimes. Here are some of the key risks of UBOs for companies:

- Exposure to money laundering: UBOs can be used by money launderers to disguise the true source of illicit funds. Concealing their ownership or control of a company can help launderers move money around the world undetected.

- Reputation risk: If a company is found to have links to individuals or entities involved in financial crime, it can devastate its reputation. This can lead to business loss, brand value damage, and other negative consequences.

- Compliance violations: Companies must comply with UBO regulations to prevent financial crime and ensure transparency. Failure to comply with these regulations can lead to significant fines, legal penalties, and other enforcement actions. Companies generally use AML software for screening their clients. Some of these software solutions also support identifying and screening UBOs.

- Financial risk: If a UBO is involved in financial crime or other illicit activities, it can negatively impact a company's financial performance. This can lead to decreased profits, loss of investor confidence, and other financial risks.

- Operational risk: If a UBO is involved in financial crime, it can also have operational implications for the company. For example, suppose the company is found to be involved in money laundering or other financial crimes. In that case, it may face increased regulatory scrutiny, disrupting operations and leading to significant costs.

How to Control UBOs?

Checking UBO is an important aspect of AML/CFT compliance, as beneficial ownership information helps to identify the true owners of a business or organization and assess their potential risk for money laundering or other financial crimes. Here are some steps to follow when checking UBO:

- Obtain the necessary information: The first step in checking UBO is to obtain the necessary information from the business or organization. This typically includes the company's registration documents, ownership records, and any other relevant documentation. Compliance officers should conduct Know Your Business procedures before UBO checks.

- Identify the UBO: Once you have obtained the necessary information, you can begin to identify the UBO. This is the person or group of people who ultimately own or control the business or organization. In some cases, the UBO may be straightforward to identify, while it may require more investigation in others. AML software for KYB can support this process.

- Verify the UBO's identity: Once you have identified the UBO, it is important to verify its identity. This may involve reviewing government-issued identification documents, such as passports or driver's licenses, and conducting background checks to ensure they do not have a history of criminal activity or involvement in illicit financial transactions.

- Assess the UBO's potential risk: After verifying the UBO's identity, you should assess its potential risk for money laundering or other financial crimes. This may involve reviewing their financial history, business activities, and any other relevant factors that could indicate potential risk.

- Document the UBO verification process: Finally, it is important to document the UBO verification process, including any steps taken to identify and verify the UBO's identity, assess their potential risk, and any other relevant information. This documentation will be important for audit and regulatory compliance purposes.

AML Software to Check UBO

Sanction Scanner's UBO check tools provide a fast and efficient way for companies to verify Know Your Business (KYB) and UBO and comply with AML/CFT regulations. By scanning owners and shareholders of companies in business deals against AML and PEP data from over 220 countries, the UBO screening tool can identify potential risks and protect your company's reputation.

With Sanction Scanner, companies can perform UBO verification in seconds, enabling them to assess potential risks and ensure quick compliance with UBO regulations. By using Sanction Scanner's UBO check tools, companies can stay ahead of the curve and prevent potential compliance violations.

To learn more about Sanction Scanner's UBO check tools and how they can help your company achieve AML compliance, you can contact us or request a demo. Our team of experts will be happy to provide you with detailed information and answer any questions you may have.